Intel Reports Record Q4 And Full Year Revenue

by Brett Howse on January 15, 2015 10:15 PM EST- Posted in

- CPUs

- Intel

- Financial Results

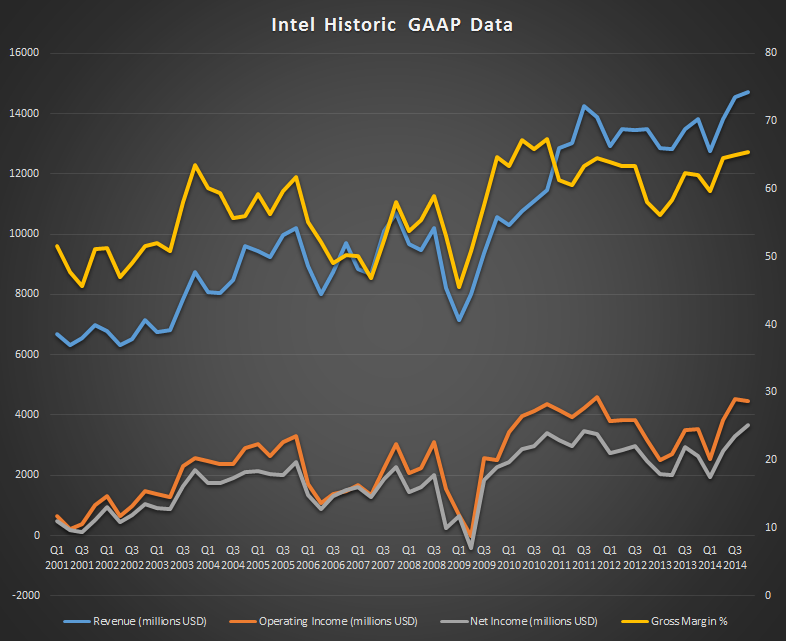

Intel released their Q4 FY 2014 results today, and they capped a record year with another record quarter. Revenue for Q4 came in at $14.7 billion, up 6% year-over-year, and for the full fiscal year 2014 revenues were a record $55.9 billion, also up 6%. Gross Margin for the quarter was 65.4%, up 3.4% over the same quarter last year, and Q4 net income was $3.7 billion, up 39% over Q4 2013. Net income for the fiscal year was $11.7 billion, up 22% over 2013. Earnings per share for the most recent quarter came in at $0.74, beating analyst’s expectations of $0.66 per share.

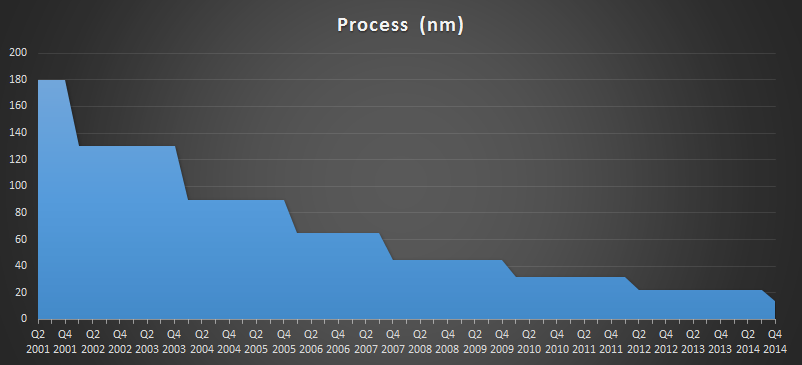

With numbers such as those, one would think Intel is on top of its game, and in the PC market it certainly is. Mobile is a different story for Intel, where it has struggled to gain traction compared to competitors using ARM’s ISA. Intel announced a contra revenue plan in November 2013, where it would subsidize the cost difference and help manufacturers implement Intel based mobile devices rather than ARM. It certainly has been successful, with Intel at the heart of many devices launched last year, including such low cost devices as the HP Stream 7. The plan has been so successful that it has cost Intel an additional $1.1 billion in operating income in Q4 alone, which brings the FY 2014 total to $4.2 billion in loss from this one division, up from the $3.1 billion loss in 2013. Clearly Intel has work to do in order to become cost competitive in this space, and they are likely hedging their bets on their 14 nm process which has just come on-line and the next generation Cherry Trail Atom core.

Looking at the individual groups, the PC Client Group had revenue of $8.9 billion, which was up 3% over the previous year. Volume was up 6%, but average selling price (ASP) was down 2%. Desktop platform volumes were down 1% with a flat ASP, and notebook platform volumes were up 11% with ASP down 3%. As compared to last quarter, revenue was down 3%, platform volumes were down 5%, and ASP was up 3%. While industry analysts IDC and Gartner debate whether the PC slowdown has slowed or rebounded, Intel’s numbers seem to indicate that 2014 was a much better year than was originally projected for the PC market.

The Data Center Group had revenue of $4.1 billion for Q4, which is up 25% year-over-year. Platform volumes were up 15% and ASP was up 10% year-over-year. Quarter-over-quarter, revenue was up 11% and volumes were up 5%, with ASP up 7%. The Data Center Group has been very strong this year, and now accounts for almost 30% of Intel’s revenue. The Xeon line is very strong right now, especially when data centers are often power constrained. Competition from ARM based alternatives is in the early stages, but it will be a tough market to penetrate at the moment.

Internet of Things was all the rage at CES this year, and Intel’s IoT group had revenue of $591 million, up 10% as compared to last year, and up 12% from the previous quarter.

The previously mentioned Mobile and Communications group actually had negative revenue for the quarter, coming in at negative $6 million, which is down from $1 million in revenue last quarter.

Software and services had revenue of $557 million, down 6% year-over-year and flat as compared to Q3.

The “other” group had revenue of $617 million, up 23% over Q4 2013, and up 7% over last quarter.

| Intel Q4 2014 Financial Results (GAAP) | |||||

| Q4'2014 | Q3'2014 | Q4'2013 | |||

| Revenue | $14.721B | $14.554B | $13.834B | ||

| Operating Income | $4.453B | $4.918B | $3.549B | ||

| Net Income | $3.661B | $3.317B | $2.625B | ||

| Gross Margin | 65.4% | 65.0% | 62.0% | ||

| PC Group Revenue | $8.871B | -3% | +3% | ||

| Data Center Group Revenue | $4.091B | +11% | +25% | ||

| Internet of Things Revenue | $591M | +12% | +10% | ||

| Mobile Group Revenue | -$6M | -700% | -102% | ||

| Software and Services Revenue | $557M | 0% | -6% | ||

| All Other Revenue | $617M | +7% | +23% | ||

The big story for Q4 was the availability of the first 14 nm parts, with Core-M devices being launched later in the quarter. The Core-M parts are the very low power offerings though (around 5 watts) and the U series 15-28 watt parts just launched at CES last week. 22 nm was alive for a bit longer than Intel would have hoped, and hopefully the 14 nm delays do not impact the next generation Skylake CPUs.

Outlook for Q1 2015 is revenue of $13.7 billion, plus or minus $500 million, which is down 7% from Q4 2014. Intel says this is normal due to the average seasonal decrease for the first quarter. Gross margin for Q1 is pegged at 60%, which is down 5.4% from Q4, and this is due to higher platform costs for 14 nm products, lower volumes, factory start-up costs, and Skylake pre-qualification costs. Intel is projecting revenue for 2015 to grow in the mid-single digits, and an overall gross margin of 62%.

2014 was a fantastic year for Intel, with record revenues overall. The mobile sector is still a sore spot, and there have already been some changes there with mobile being moved into the PC unit. Many people expected that to be done to mask the losses, but Intel did report it as a separate group for Q4, although that may change in the future. More Core like processors in mobile may be exactly what Intel needs, with higher IPC and the ability to run at a lower clock speed due to good IPC.

Source: Intel Investor Relations

38 Comments

View All Comments

stefstef - Thursday, January 15, 2015 - link

a nice value for the stock portfolio. intel ignored the lowpower gadget market for years. just to come back now with a decent and complete setup for these markets. smells like success here.Samus - Thursday, January 15, 2015 - link

Yep. It's possible we'll all have Intel SoC's in our phones in the next few years. as great as ARM is, the only licensee that can compete with Intel in manufacturing is Samsung, and as great as Exynos is on paper, Apple's SoC's still trump it (and everyone else) in raw performance with a fraction of the cores. Given Apple and Intel's close relationship, it isn't far fetched to see Intel minting Apple SoC's in the future, ARM or otherwise.melgross - Friday, January 16, 2015 - link

Qualcomm makes almost 80% of the SoC's for Android now, and I see no reason why that will change in the near, or mid future. Samsung makes crappy SoC's. I'd be willing to bet their costs are higher than Qualcomm's. One would think it odd that Samsung finds it necessary to use Qualcomm chips in more than half of their own phones, and they find it almost impossible to sell them to anyone else. Apple has been, by far, the largest beneficiary of Samsung's chip manufacturing, estimated to have been, when they only used Samsung, 65% of Samsung's capacity. Most of the rest of those chips being chips Samsung themselves use, but again, only for some of their devices, and rarely the high end ones sold in N America, or places where the best performance is demanded.Remember that Samsung only has a design license, not an architecture license, as Apple, Qualcomm and Nvidia has, so they can't design better chips than those designs ARM provides.

Flunk - Friday, January 16, 2015 - link

Qualcomm has a short-term issue now, they don't have a 64bit version of their Krait cpu core.They're using ARM designs as a stop-gap but their advantage just disappeared. Nvidia may even get Denver out being Qualcomm has a 64bit Krait core.icrf - Friday, January 16, 2015 - link

Qualcomm's advantage has at least as much to do with a quality integrated modem as it does a better performing CPU, so I think moving from Krait to stock cores for a generation or two won't be the end of the world for them. I would like to see Denver in more devices, though.Penti - Saturday, January 17, 2015 - link

Qualcomm has some advantage, Broadcom, TI, and ST-E exited the market. But good modems/radios are coming now (for LTE) from Intel, Samsung and others. A good Application Processor with a Qualcomm, Intel or Samsung modem can get pretty far at the moment. Hell even Denver is used with Qualcomm modems. Adreno has been pretty solid but both ARM and ImgTec solutions are quite good at the moment. Intel is getting there too. Samsung radios does 3x20 aggregation, Intel does have a decent cat 6 lte-a solution. Denver plus Icera might be a tougher sell. Icera as a discrete modem is really only in Nvidia's own products.Samsung collaborates with ARM through a foundry program, which means they do adapt the processors for it's processes and are actually involved deeply developing the IP and can do plenty of optimizations, but don't change the architecture. Integration and support matters, and Qualcomm isn't using their own arch with 64-bit yet. Nothing is stopping Samsung going custom though.

Samsung uses chips form different vendors and it's really another part of the conglomerate that does semiconductor stuff, it's not just for in-house use. We have Intel, Qualcomm, Samsung at Samsung phones and tablets already. Wouldn't be surprised to see more vendors there. They want to sell stuff, they also sell LCD and OLED displays, batteries, memory and NAND in this field and to far more customers then to themselves.

Krysto - Friday, January 16, 2015 - link

Your comment makes no sense and is all over the place. You're basically implying one one side that ARM isa sucks, and then praising Apple's SoC - which is based on ARM - for how great it is.News flash. Apple's ARM chips can beat Atom on an older process than what Intel uses. What does that say about Atom's IPC? That it's pretty crappy, right?

ws3 - Friday, January 16, 2015 - link

Seamus doesn't say or even imply anything bad about the ARM ISA.His point is that only Intel has both top-notch process and top-notch SoC design. Samsung has process, but not design. Apple has design but not process.

Samus - Friday, January 16, 2015 - link

Atom's IPC is older than Apple's SoC engineering department. Way to go, you win the internet.darkich - Saturday, January 17, 2015 - link

And it's not just Apple.Krait and Cortex also had it beaten, or at least on par, on inferior process.

And let's not forget the GPU architecture where Intel is embarrassingly bad compared to Imagination, Qualcomm, ARM and Nvidia GPU architectures.